This is my final take on Roth vs. Traditional 401k in which I extend the previous model to include two new variables:

- a different tax rate

for money withdrawn from 401k (the expectation is that you will be in a lower tax bracket during retirement) and

- a variable

to denote the expenses in a year. These expenses need to be deducted from the amount that is invested in the ordinary non-tax sheltered account.

with these two variables, the new calculations for Roth vs. traditional are as follows:

Roth 401k

Total =

where:

Traditional 401k

Total =

where:

Let’s see what we get if we subtract the two:

Now recall

simplifying:

For

This looks like a linear relationship in

- your current tax bracket

- your expected tax bracket during retirement

- expected rate of return on investment

- time to retirement

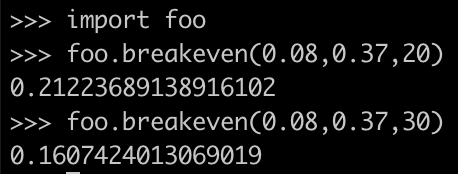

We can write a small function that gives us the breakeven point when both Roth and Traditional will give same return:

Let’s see what it gives:

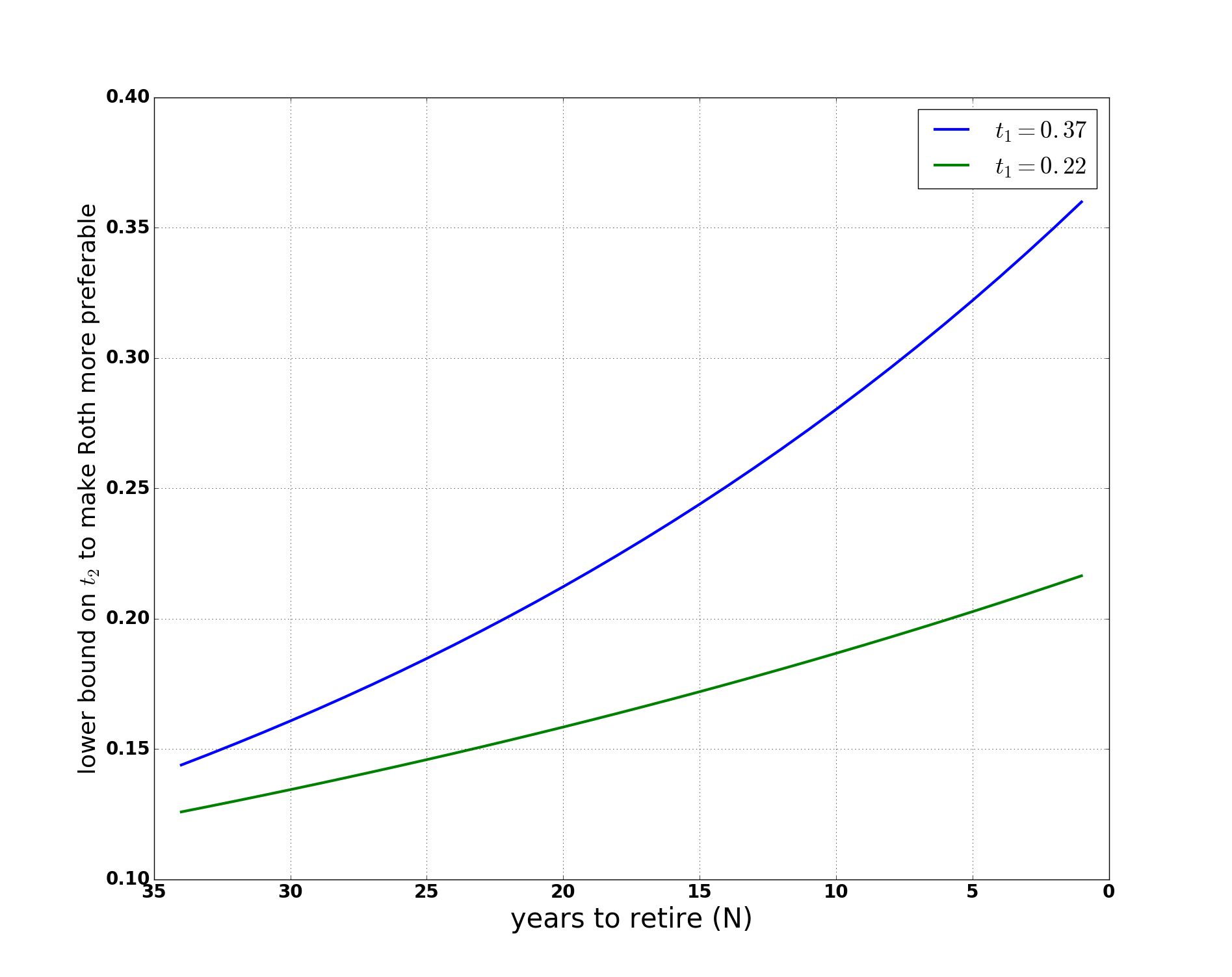

Plot of breakeven point vs. N (# of years till retirement) with

Enough math. Can I get it in English please? Investing in Roth makes sense if you are young (i.e., N ↑) or in a low tax bracket (

Conclusion: Go Roth when you are young and switch to Traditional 401k once you cross 40-45 years of age. For most people that represents mid-point of their career. Thus, in other words, the conclusion is to split evenly between Roth and Traditional 401k. Choose Roth for first-half of your career and Traditional for the second half.

of course, again all this is just bookish exercise for fun. Code is here.