There is a subtle bug in my original post on Roth vs. Traditional 401k. The bug being that in Roth 401k, we pay taxes upfront but we still get to invest full contribution amount that grows tax-free. The bug is so subtle that let’s do another analysis that will make it clear. Let

Roth 401k

We start with

Total =

Traditional 401k

We start with

Total =

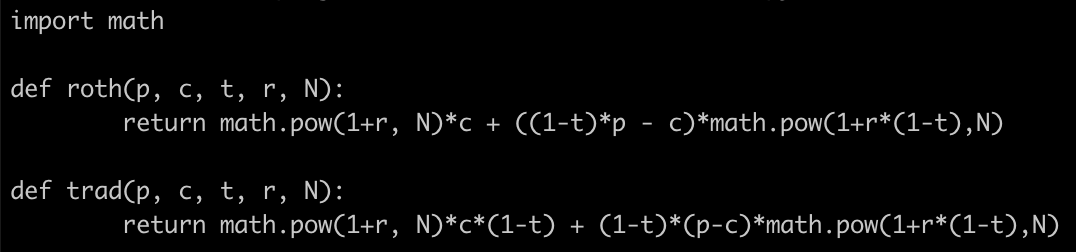

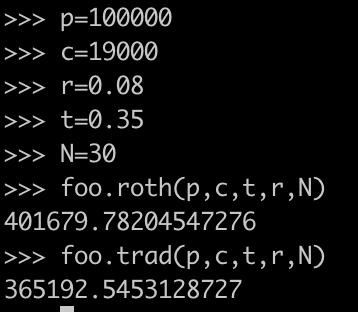

The total amount we end up with is not the same in the two cases. I wrote a small script to compute the two totals

when I run this script:

so Roth seems to be better. But beware, this is just bookish exercise that assumes